Where Renting Beats Buying: The U.S. Cities and Neighborhoods Where Renters Save the Most

The financial advantages of buying versus renting your home fluctuate with changing economic conditions. But they also depend on the location of the property, as our new report illustrates.

For those who can afford a house, buying can help build equity as you pay off your mortgage. But buying, which involves a deeper commitment, may entail higher monthly costs including property tax and insurance, and can be harder to manage if fluctuating interest rates raise your monthly repayments.

To help young families zero in on where their dollar can go the furthest, online lender NetCredit analyzed and compared average rental prices and average monthly homeownership costs (comprising principal and interest on the mortgage, property taxes and home insurance costs) across 268 major U.S. cities and 4,241 neighborhoods.

Key Findings: Renting vs. Buying

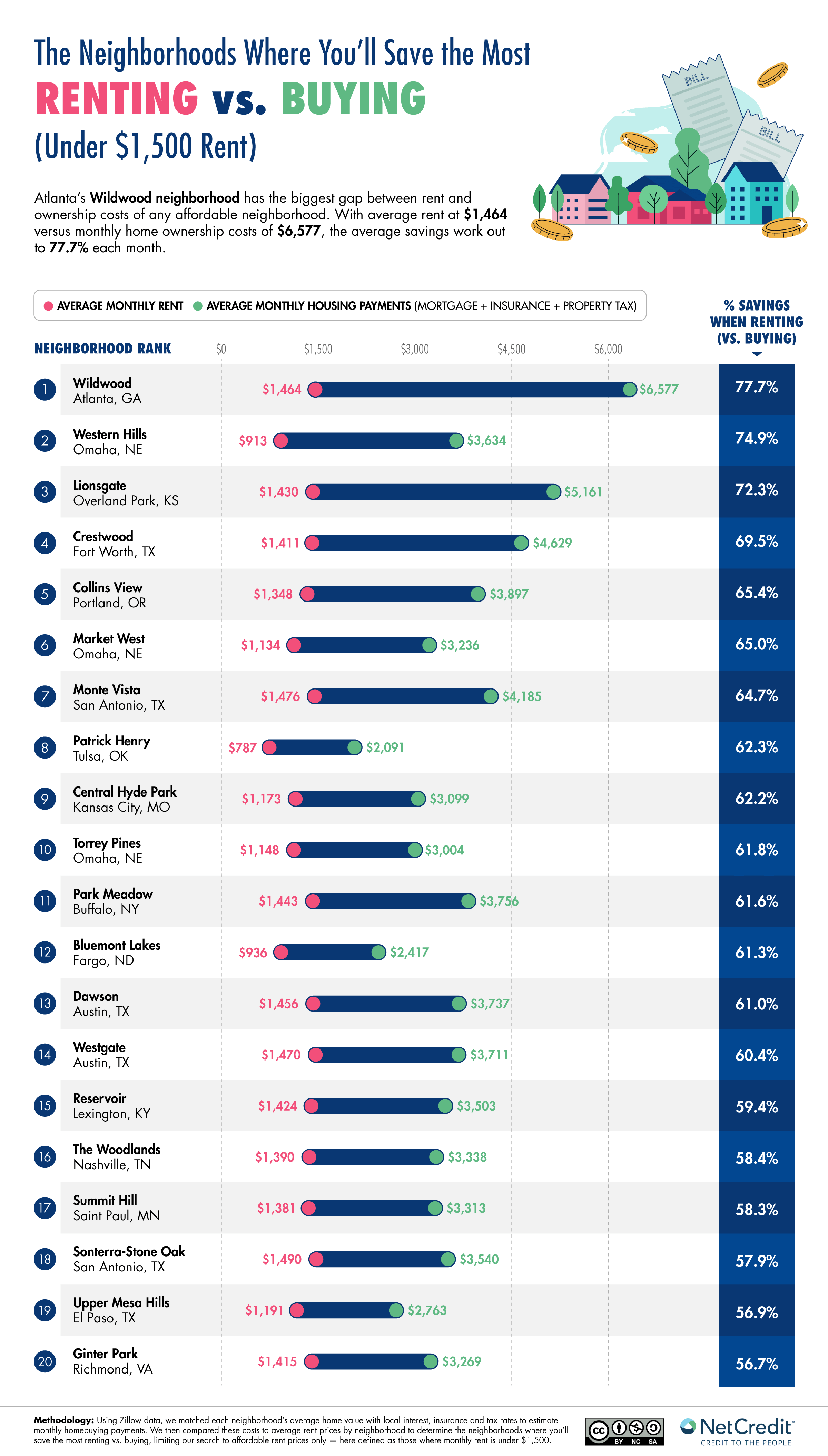

- Wildwood in Atlanta, Georgia, is the affordable neighborhood (rent below $1,500/month) where renters save the most vs. buying — savings of 77.7%.

- Omaha, Nebraska, claims three spots in the top 20 most affordable neighborhoods for renters — more than any other city in that category.

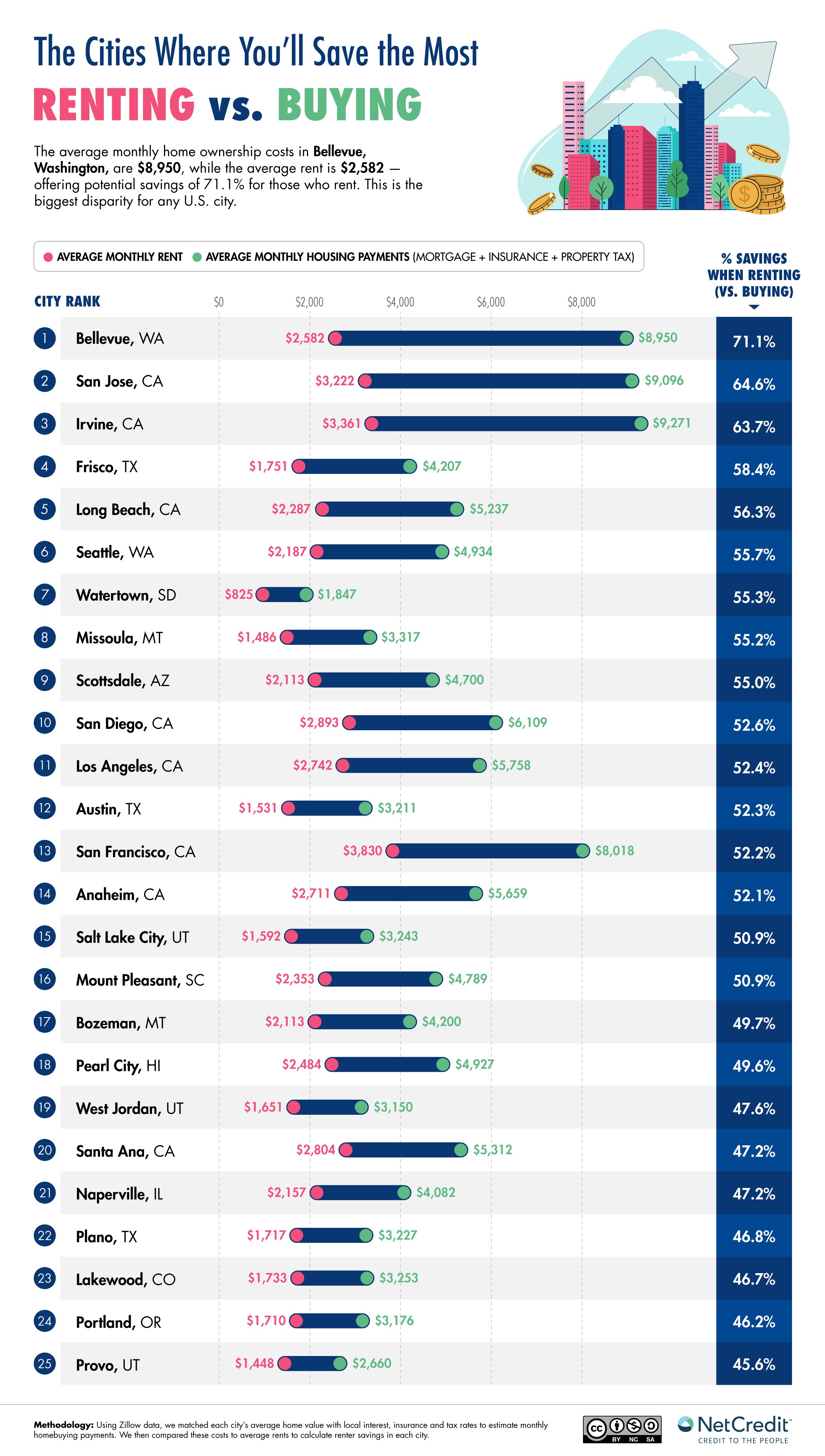

- Bellevue, Washington, is the best city for renters in our study, with savings of 71.1% when comparing the average monthly rent of $2,582 against homeownership monthly payment costs of $8,950.

- Nine of the top 25 cities where renters save the most are located in California, Texas or Washington.

We found a wide range of locations where renters can save, from budget-friendly Midwestern cities to upscale West Coast neighborhoods where the gap between renting and buying is particularly pronounced.

Atlanta’s Wildwood neighborhood is the most affordable for renters compared to buyers.

For those prioritizing affordability, the neighborhoods below offer some of the strongest cases for renting. Each was found to have an average monthly rent of no more than $1,500.

Topping the list is Wildwood in Atlanta, Georgia, where renters pay an average of $1,464 per month compared to the $6,577 the average homeowner faces, giving a saving of 77.7%. Wildwood is a secluded, peaceful neighborhood popular with young families who may appreciate a chance to save while collecting the funds for a deposit.

Close behind is Western Hills in Omaha, Nebraska, where an average monthly rent of just $913 represents a 74.9% saving over the average monthly buying cost of $3,634 — the homes in Western Hills are recently built and tend towards the luxury market.

Texas also makes a strong showing with neighborhoods in Fort Worth (69.5%), San Antonio (64.7% and 57.9%), Austin (61% and 60.4%) and El Paso (56.9%) all appearing in the top 20, reflecting this state’s current rental market.

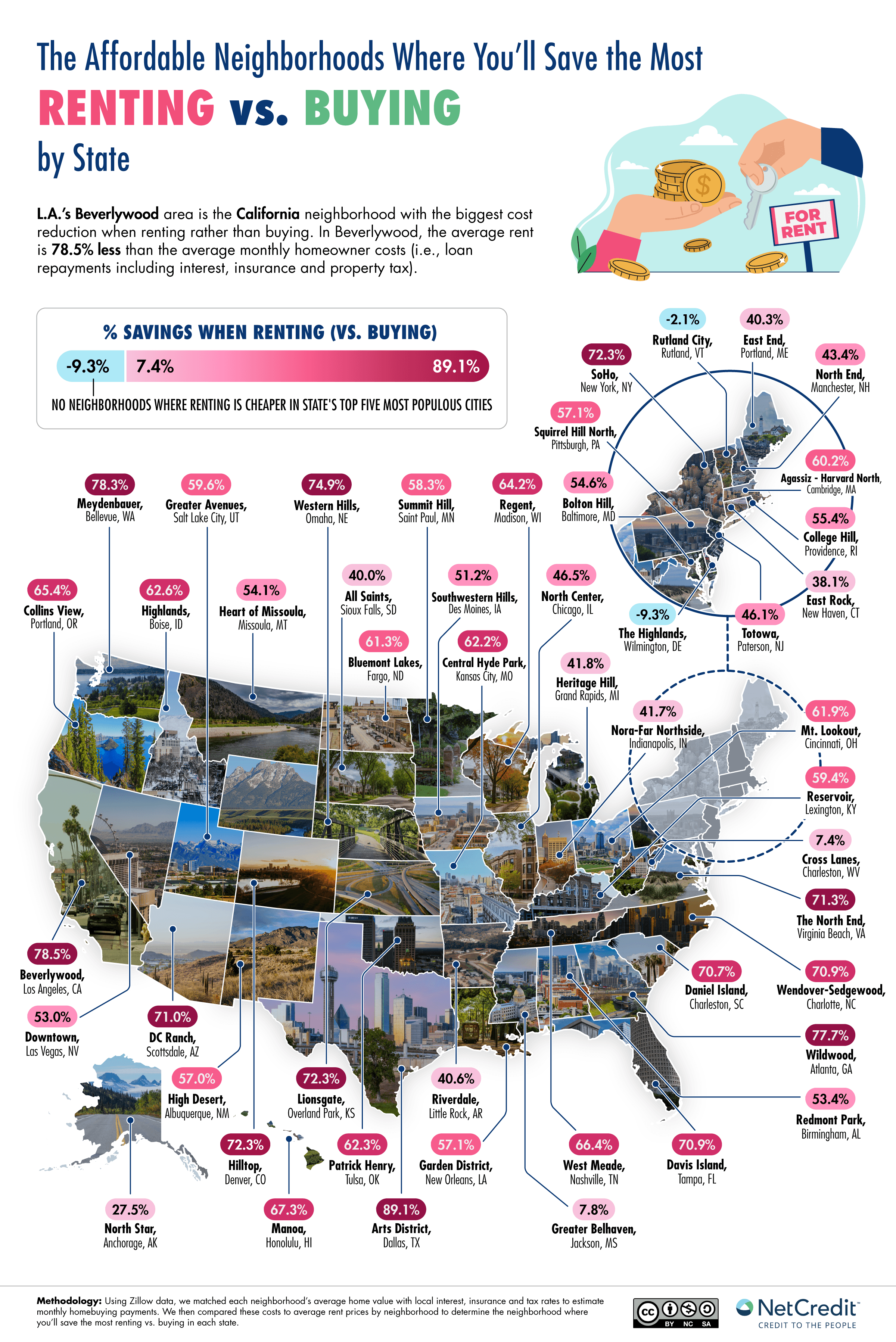

The best neighborhood for renters in every state.

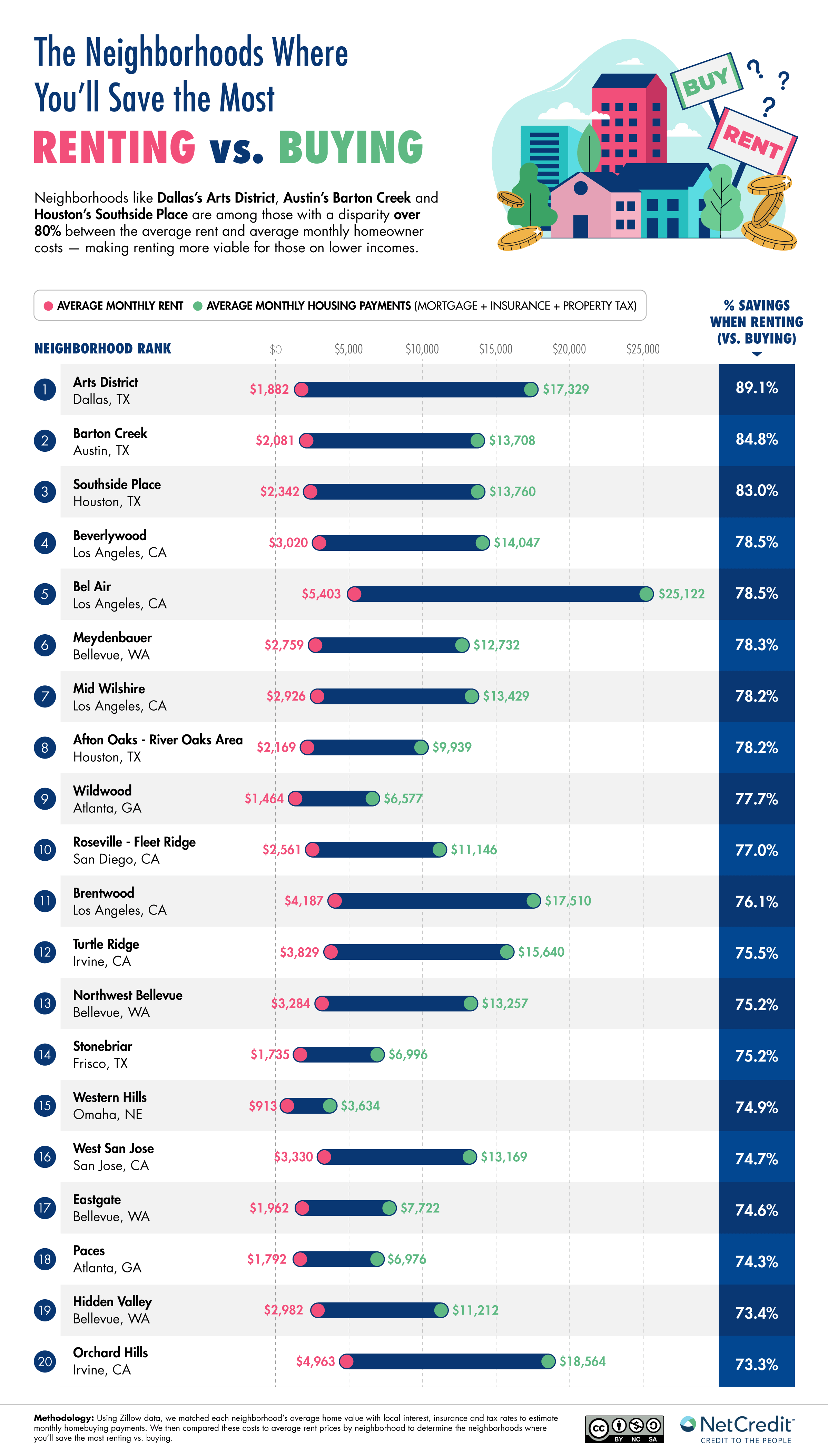

We found that nearly every state has at least one neighborhood where renting offers a significant financial advantage over buying, with the Arts District in Dallas making the strongest case for renting — with an average monthly rent of $1,882 and a homeownership cost of $17,329, renters in this Dallas neighborhood can save up to 89.1%.

Only two states didn’t have neighborhoods where renting was cheaper than buying in their top five most populous cities: Vermont and Delaware.

In Delaware’s case, all 12 qualifying neighborhoods we looked at are in the city of Wilmington, where residents have recently made the news for protesting rising rent prices. Mayor John Carney has earmarked $16 million in incentives for developers to prioritize affordable housing for the lowest earners.

At the city level, West Coast renters save the most.

Next, we identified the cities with the highest average gap between average rental costs and homeownership costs. We found the gap between renting and buying is most pronounced among several more expensive cities where strong demand for housing has pushed home prices well above rental rates.

At the top of the list is Bellevue, Washington, with an average monthly rent of $2,582 against average monthly homeownership costs of $8,950, giving average savings of 71.1%. However, you may face higher rental costs for two- and three-bedroom homes, for which rents are rising across the Seattle-Tacoma-Bellevue metropolitan area, while house prices remain stable despite an increase in available properties.

More moderately priced cities in the Midwest and the Mountain West also make a strong case for renting over buying. In Watertown, South Dakota, renters pay an average of just $825 per month and save 55.3% over buyers. Renters in Missoula, Montana, also pay less than $1,500 in rent per month and save an average of nearly $2,000 per month over homeowners.

Upscale neighborhoods in Texas, California and Washington see huge gaps in rental vs. buying costs.

Lastly, we considered all rental properties rather than just those under $1,500 as in the section above.

We found that some of the largest gaps between renting and buying occur in upscale neighborhoods where strong demand has pushed home values far higher than rental rates. In the Arts District in Dallas, for example, the average monthly rental costs $1,882, but the average monthly cost of homeownership is a staggering $17,329. This means renters in the area are saving 89.1% over homeowners on average. Covering 20 city blocks, this is America’s “largest contiguous urban arts district” and an astonishingly lively place to live — but perhaps not for too long.

Seven out of the 20 neighborhoods with the biggest gaps are in Southern California, and four of those are in L.A. The neighborhood in L.A. where residents save the most by renting is Beverlywood.

Investing in property is a big deal in this “(almost) Beverly Hills-adjacent” neighborhood, where generations of wealthy suburbanites extensively added on to or even rebuilt their homes to add precious square footage. Today, the average rent is $3,020, and the average home mortgage price is $14,047 per month.

Making the most of renting in today’s market.

Renting offers some real benefits in many cities and neighborhoods across the U.S., and making the most of these advantages takes a little planning. Whether you’re renting by choice or circumstance, here are some ways you can get the most out of it:

1. Understand your local market.

Rental prices can vary from city to city, but also from one neighborhood to the next within the same metro. Tools like Zillow’s rental listings make comparing nearby options simple.

2. Negotiate your lease.

In markets where rental demand has softened, landlords are often more open to negotiating on price, lease length or included utilities. It’s always worth having the conversation and it just might help reduce your expenses.

3. Factor in the “cost of happiness”

It’s easy to look at a map showing one neighborhood that costs $800 and another that costs $2,000 and opt for the cheaper one. But it’s also important to factor in the price of happiness if you’re able to. If an area costs less but doesn’t have the things that make you happy, is it worth the savings?

4. Factor in the full cost of renting.

Buying a home comes with a range of expenses, but so does renting. Renters’ insurance, parking and utilities can all add up — and may stretch renters thin. Ensure you compare like-for-like when calculating the costs of different options to avoid unwelcome surprises.

5. Build your savings deliberately.

The gap between renting and buying in many of the cities we’ve analyzed is significant. If you’re able, use that gap as an opportunity to channel those savings into a high-yield savings account or investment fund. This can help you build long-term financial security while renting. Be sure to consult with a financial advisor to determine the best investment options for your specific situation.

6. Keep an eye on the market.

Housing markets evolve, and the gap between renting and buying can shift as interest rates and home prices fluctuate. Stay informed to be in a stronger position to make the right decision if your circumstances, or the market, change.

Explore the Data: Find your city or neighborhood.

Whether you’re considering whether to rent or buy, or just curious about how your area compares, use the filters and search box to find the American cities and neighborhoods where renters can save the most compared to buyers.

Methodology

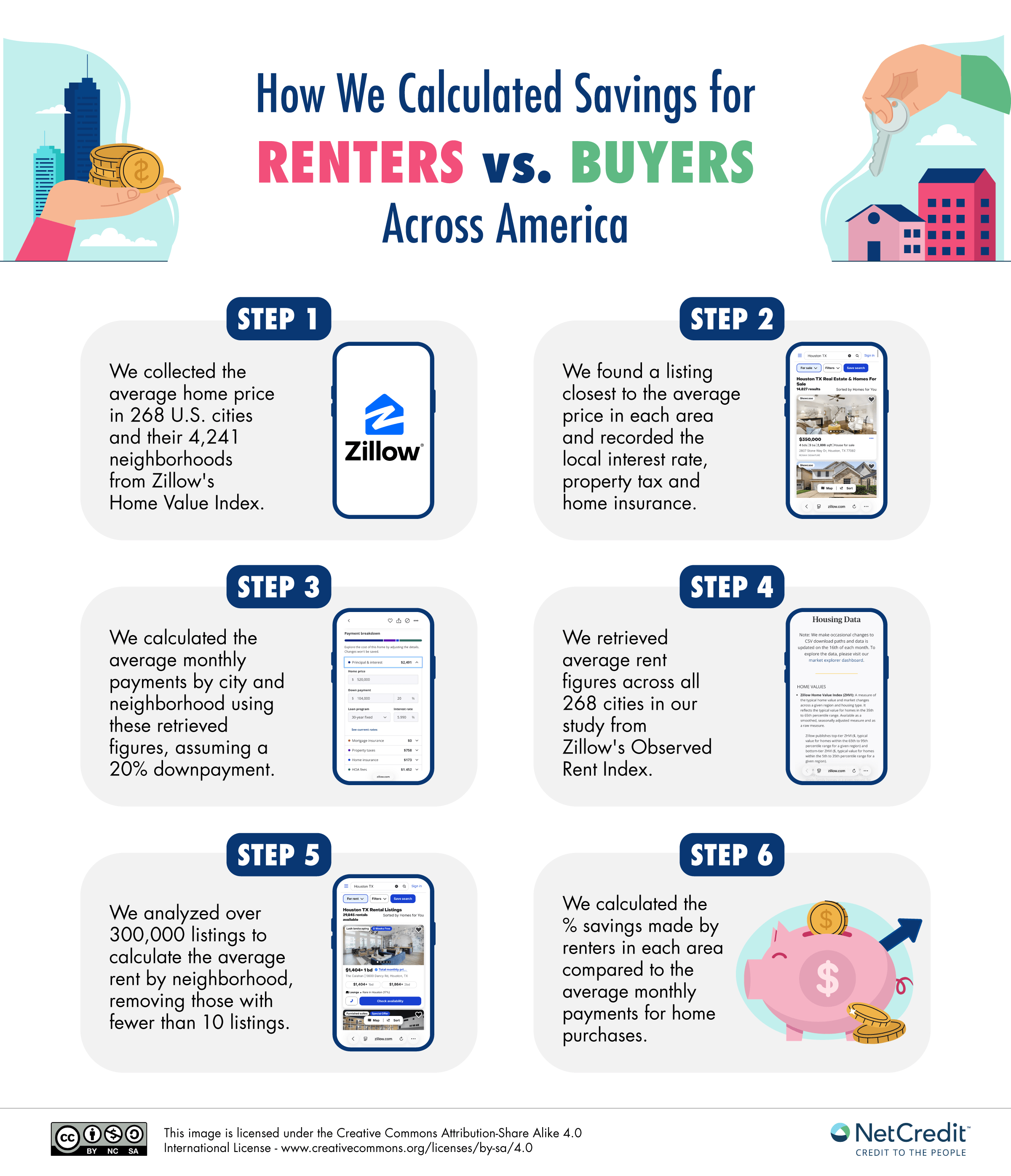

We compared average rental prices to estimated monthly homebuying payments across 268 major U.S. cities and 4,241 neighborhoods using Zillow data.

For cities, we:

- Used Zillow’s Home Value Index to determine average home values.

- Retrieved local interest rates, insurance and property taxes by identifying listings closest to each city’s average home price and recording the rates provided by Zillow.

- Calculated average monthly homebuying payments using Zillow’s calculator, assuming a 20% down payment.

- Pulled average monthly rents using Zillow’s Observed Rent Index.

- Calculated the percentage savings for renters compared to homebuying costs, excluding HOA fees.

For neighborhoods, we:

- Used Zillow’s Home Value Index to determine average home values.

- Retrieved local interest rates, insurance and property taxes by identifying listings closest to each city’s average home price and recording the rates provided by Zillow.

- Calculated average monthly homebuying payments using Zillow’s calculator, assuming a 20% down payment.

- Determined average rents by analyzing over 300,000 rental listings, excluding those below $500 and above $10,000 to remove outliers.

- Calculated the percentage savings for renters in each neighborhood compared to homebuying costs, excluding HOA fees.

Data is accurate as of March 2026.

DISCLAIMER: This content is for informational purposes only and should not be considered financial, investment, tax or legal advice.